By Ajita Dash & Kavya Thapliyal

Limited Liability Partnership (LLP) has become a preferred form of organization among entrepreneurs in India. An LLP incorporates the benefits of a partnership firm as well a company. As the name suggests, an LLP is a partnership firm established by a number partners who enter into an agreement to carry out business under a common seal. Moreover, the partners of an LLP have limited liability and the LLP has perpetual succession just like a company.

The concept of the Limited Liability Partnership (LLP) was introduced in India in 2008. The Limited Liability Partnership Act, 2008 regulates the LLPs in India. A minimum of two partners are required to incorporate an LLP. However, there is no upper limit on the maximum number of partners. It is also interesting to note that there is no minimum Authorized Capital requirement for an LLP.

Among the partners, there should be at least two Designated Partners who must be natural persons, and at least one of them should be resident in India. The rights and duties of Designated Partners are governed by the LLP agreement. They are directly responsible for the compliance of all the provisions of the LLP Act, 2008 and clauses specified in the LLP agreement.

LLP Registration Process

LLPs are registered in a similar manner as Private Limited Companies. Certain requirements have been provided by the LLP Act, 2008 for the registration of an LLP in India. The complete process of registration takes approximately 10-15 business days, though the timeframe may differ depending on the workload of the Registrar of Companies. The steps to be taken in order to register an LLP have been mentioned here:

- STEP 1: Obtaining Digital Signature Certificate (DSC)

Before initiating the process of registration, an application must be made to obtain the Digital Signatures (DSC) of the Designated Partners of the proposed LLP. This is because all the documents for LLP are filed online and are required to be signed digitally.

- STEP 2: Applying for Designated Partner Identification Number (DPIN)

Once all the designated partners have their DSCs, an application for the Designated Partner Identification Number (DPIN) of all the designated partners or those intending to be Designated partners of the proposed LLP is submitted. A scanned copy of required documents needs to be attached to the form. The form should also be signed by a Legal Professional. Company Secretary or Chartered Accountant in full-time practice.

- STEP 3: Name Approval

RUN-LLP (Reserve Unique Name-Limited Liability Partnership) is filed for the reservation of the name of the proposed LLP which shall be processed by the Central Registration Centre. The registrar will approve the name only if the name is not objectionable in the opinion of the Central Government and does not resemble any existing partnership firm, an LLP. a body incorporate or a trademark.

- STEP 4: Incorporation of LLP

The form used for incorporation is FiLLiP (Form for incorporation of Limited Liability Partnership) which shall be filed with the Registrar who has jurisdiction over the state in which the registered office of the LLP is situated. If the proposed name is approved by the MCA, then it shall be filled as the proposed name of the LLP. Once the application for incorporation has been submitted along with requisite fees, the application shall be approved by the ROC and the Certificate of Incorporation shall be sent to the applicant within the specified time period.

Post-Registration Compliances

After the registration of a Limited Liability Partnership (LLP) in India, there are several post-registration compliances that LLPs need to adhere to. Here are some of the key post-registration compliances:

LLP Agreement

Immediately after Incorporation of the LLP, the Partners of a Limited Liability Partnership are required to execute an LLP Agreement and a copy has to be filed with the Registrar of Companies within 30 days of the incorporation.

Application for Permanent Account Number (PAN)

Every LLP has to obtain a Permanent Account Number (PAN) from Income tax department, Government of India. PAN is an identification number for every tax payer under the Income Tax Act, 1961. For obtaining a PAN, the LLP has to make an application with a copy of its Certificate of Incorporation.

Application for Tax Deduction and Collection Account Number (TAN)

Also, every LLP planning on having employees in the near future has to obtain a Tax Deduction and Collection Account Number (TAN) from Income tax department, Government of India. Certain categories of payments require Tax Deduction at Source (TDS) and the tax so deducted must be remitted to the government. To enable the TDS remittance, Tax Deduction and Collection Account Number (TAN) is required.

Opening Bank Account in the LLP’s Name

After incorporation of the LLP, it is necessary to open a Current Account in the name of the LLP with any Bank in India. All the transactions in the name of the LLP should be transacted through the LLP Bank Account only.

Books of Accounts of LLP

Every LLP has to prepare and keep the books of account in double entry system of accounting on accrual basis. The LLP has to maintain the Books of Accounts of all receipts payments and to comply legal requirements under Companies Act and other various laws. The books of accounts and financial statements shall give a true and fair view of the state of the affairs of the LLP, including its branch office or offices.

Infusion of Initial Capital by the Partners

The initial partners of LLP have to bring the amount of capital contribution as stated in the LLP Agreement at the time of LLP registration within 60 days of incorporation.

Appointment of Auditors

Every LLP whose capital contribution exceeds Rs. 25 lakhs or annual turnover exceeds Rs. 40 lakhs has to get the accounts audited by a Chartered Accountant in Practice. There is no mandatory audit requirement for other LLPs.

Goods and Services Tax (GST) Registration

Every business with annual turnover exceeds Rs. 40 lakhs (Service providers 20 lakhs) is required to GST Registration under Goods and Services Tax (GST) Act and Rules. It is not mandatory to obtain GST immediately after incorporation of the LLP. The LLP can obtain this registration as and when required.

Trademark Registration

Registering a Company or LLP with a name does not provide complete protection to the name or brand name. The protection of Company /LLP name under the Companies Act / LLP Act is limited to the extent that another Company or LLP will not be registered with the same or a closely-resembling name. Thus, registering a Trademark shall ensure that no other entity can replicate the Company/LLP’s name in their own business.

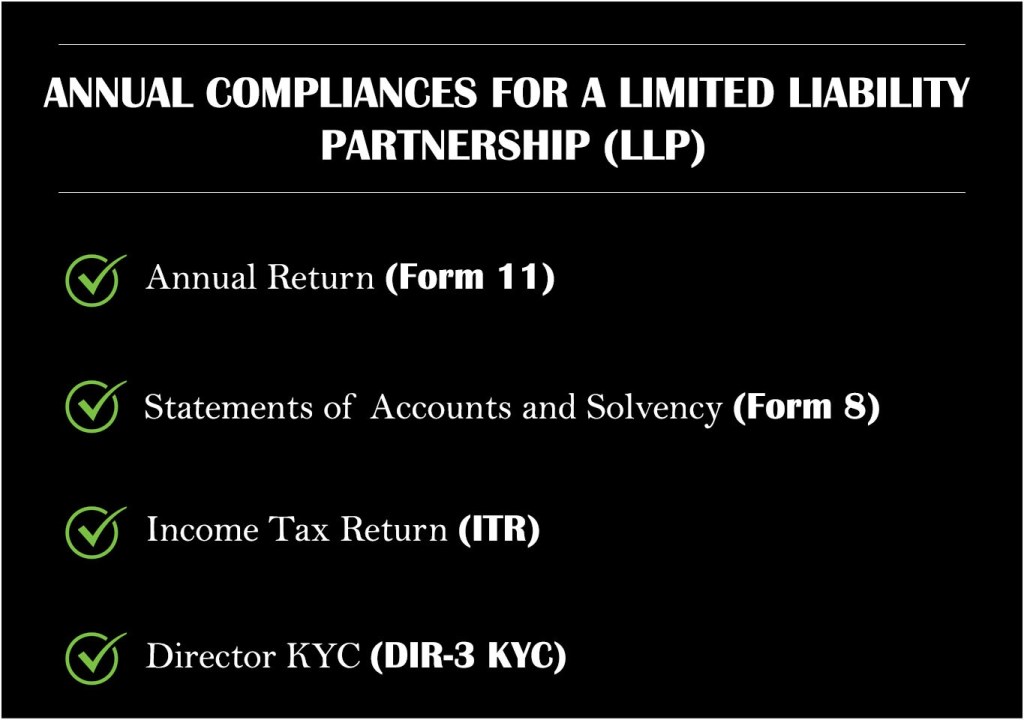

Annual Compliances

Every Limited Liability Partnership (LLP) must fulfil certain annual compliances which typically include several statutory requirements that must be fulfilled on an annual basis to maintain compliance with the regulations. Here’s a general overview of the annual compliances for LLPs in India:

Annual Return (Form 11)

All LLPs are required to file an annual return in Form 11 with the Registrar of Companies (ROC) within 60 days from the end of the financial year (on or before 30th May). This form shall include details such as the principal place of business, partners’ details, and turnover.

Statements of Accounts and Solvency (Form 8)

LLPs must prepare and file their annual Statements of Accounts and Solvency in Form 8 with the ROC within 30 days from the end of six months of the financial year (on or before 30th October). The financial statements consist of the Balance Sheet, Profit and Loss Account, and Statement of Solvency.

Income Tax Return (ITR)

All LLPs are required to file their income tax returns (ITR-5) annually. The due date for filing income tax for LLPs is on or before 31st July if tax audit is not mandatory for the entity. However, if audit is mandatory for a particular LLP, then the due date for filling the ITR is on or before 30th September.

Director KYC (DIR-3 KYC)

Every Director of a Company or Partner of an LLP who has been assigned a DIN/DPIN before 31st of March of a particular year, is compulsorily required to file the DIR-3 KYC form on or before 30th of September of the following financial year. This form must be filed annually by the Directors/Partners in order to retain their DIN/DPIN.

Difference between Partnership Firm and Limited Liability Partnership (LLP)

There comes a point in the life of every entrepreneur where they must make a decision on the type of business structure that shall be most suitable for them. A great deal of confusion arises when comparing Partnership Firms and Limited Liability Partnerships. Though both the structures are extremely similar in nature, yet there are several crucial differences between the two which set them apart from each other. Under a traditional “Partnership Firm”, every partner is liable, jointly with all the other partners and also severally for all acts of the firm while he is a partner. However, under LLP structure, liability of the partner is limited to his agreed contribution. Further, no partner is liable on account of the independent or unauthorized acts of other partners, thus allowing individual partners to be shielded from joint liability created by another partner’s wrongful acts or misconduct.

The key differences between LLP and partnership firms in India are as follows:

| Particulars | LLP | Partnership Firm |

| Governing Law | The Limited Liability Partnership Act, 2008 governs LLPs. | The Indian Partnership Act, 1932 governs partnership firms. |

| Registration | The registration of an LLP as per the LLP Act is mandatory. | The registration of a Partnership Firm under the Indian Partnership Act is voluntary. |

| Registering Authority | An LLP should submit the registration form and all the subsequent e-forms to the Registrar of Companies. | The Firm must submit the Partnership Firm registration form and other subsequent forms to the Registrar of Firms. |

| Creation | An LLP is created by law. | A Partnership Firm is created by contract. |

| Binding Document | The LLP Agreement is the charter document of an LLP. | The Partnership Deed is the charter document of a Partnership Firm. |

| Separate Legal Entity | An LLP has a separate legal entity under the law. | A Partnership Firm has no separate legal status apart from its partners. |

| Liability of Partners | A partner’s liability in an LLP is limited to the extent of their capital contribution to the LLP. | A partner of a Partnership Firm has unlimited liability. |

| Perpetual Succession | An LLP has perpetual succession, which means its existence is not affected when a partner joins or leaves. | A Partnership Firm does not have perpetual succession, and its existence depends upon the will of its partners. |

| Maximum Partners | There is no limit on maximum partners in an LLP. | The maximum number of partners in a Partnership Firm is limited to 100 partners. |

| Common Seal | An LLP has a common seal which denotes the signature of an LLP. The common seal is used to sign documents. | There is no concept of a common seal in a Partnership Firm. The authorised partner must sign the documents. |

| Annual Compliances | An annual statement of accounts, solvency, and yearly returns must be filed with the Registrar of Companies. | In a Partnership Firm, no annual filings are required to be made to the Registrar of Firms. |

| Taxation | An LLP is taxed as a separate legal entity at the rate of 30% of their annual profits. | A Partnership Firm is not taxed as a separate entity, each partner is taxed as per their share of business profits. |

| Compliance Burden | LLPs are required to file annual reports with the Registrar of Companies and are required to maintain extensive records, thus, have comparatively more compliance burden than a Partnership Firm. | The legal compliances required are minimal for a Partnership Firm. |

| Management and Administration | Designated Partners are required to take care of the management, administration and compliances of an LLP. | The Partners take care of the management and administration of a Partnership Firm. |

| Name of the Firm | An LLP may choose any name for their firm; however, it must be followed by the term “LLP” at the end. | Firm may adopt any chosen name. |

| Contractual Obligations | An LLP can enter into a contract in its own name. | A Partnership Firm cannot enter into a contract in its own name. A partner may be assigned as an agent to enter into contracts on behalf of the Firm. |

| Ownership of Assets | An LLP may acquire assets in its name. An LLPs assets are separate from its partner’s individual assets. | All assets belonging to the firm are jointly owned by the partners. |

| Foreign Ownership | A foreign national may form an LLP in India with an Indian national. | Foreign nationals are not permitted to form a partnership firm in India. |

| Auditing of Records | Only those LLPs whose turnovers are over 40L must get their accounts audited annually under the Limited Liability Partnership Act, 2008. | All Partnership Firms must mandatorily have their records audited under the Income Tax Act, 1961. |

| Compromise and Amalgamation | An LLP may enter into a compromise with its Creditors/Partners as well as amalgamate/merge with another LLP. | A Partnership Firm can neither enter into a compromise with its Creditors/Partners nor amalgamate/merge with another Partnership Firm. |

| Dissolution | An LLP may be dissolved voluntarily or by an order of the National Company Law Tribunal. The dissolution procedure must be initiated with an application before the ROC. | Partnership Firms may be dissolved by an agreement between the partners, court orders, mutual consent, insolvency, etc. |

| Who is it Suitable for? | An LLP is suitable for individuals who want to enjoy the benefits of limited liability and conduct their business activities as a separate legal entity under a common seal. | A Partnership Firm is suitable for individuals who are collectively agreeing to commence their business activities without excessive legal compliance burden and are open to accepting unlimited liability for the same. |

Incorporate your LLP today!

With the flexibility of a partnership and the advantage of limited liability for its partners, LLPs offer a conducive environment for business growth and sustainability. The LLP registration process involves several steps, including obtaining digital signatures, applying for partner identification numbers, and securing name approval from the Central Registration Centre. Post-registration, LLPs must comply with various statutory requirements, such as executing an LLP agreement, obtaining PAN and TAN, opening a bank account, and maintaining proper books of accounts. Additionally, they need to adhere to tax regulations, obtain necessary registrations like GST and professional tax, and fulfil capital infusion and audit requirements as per the LLP Act.

Overall, the LLP framework offers a robust platform for entrepreneurial ventures to thrive while ensuring legal compliance and protection for all stakeholders involved. Whereas, Partnership Firms carry on their business activities without a common seal and with unlimited Liability. It depends on the proprietors to make an informed decision regarding the appropriate model of organisation.

The team of experts at Advoke Law actively assist the proprietors of new businesses decide upon the most-suitable business structure and get registered as Sole Proprietorships, Partnership Firms, Limited Liability Partnerships, Private Limited Companies and One-person Companies. Feel free to contact us to schedule a free consultation today!